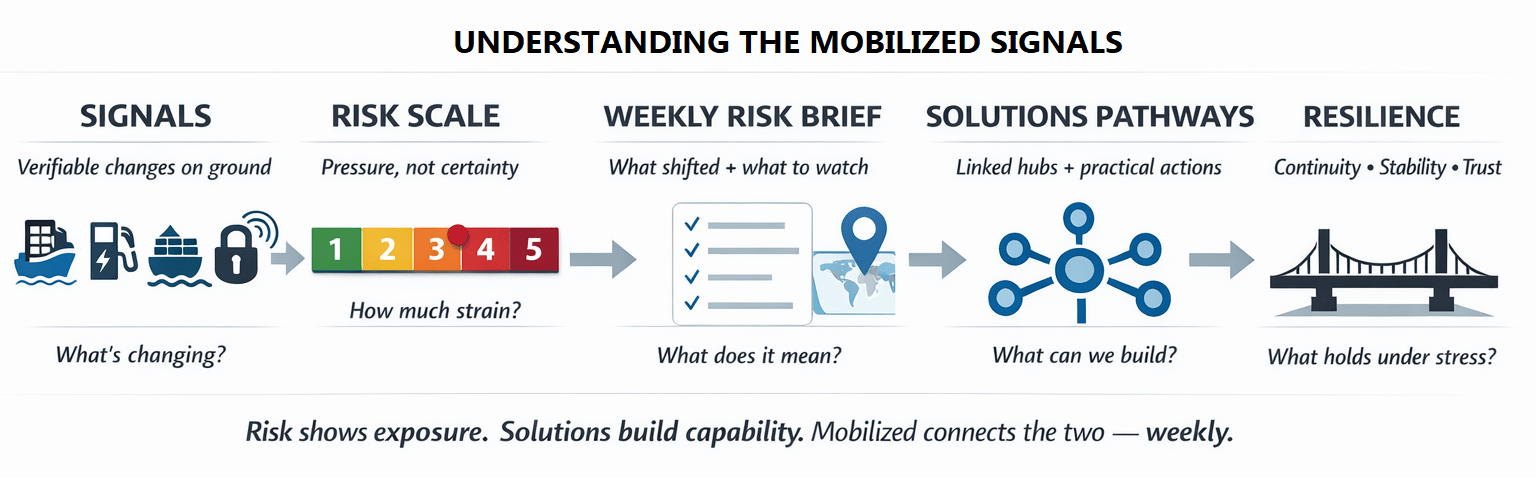

🚨 MOBILIZED NEWS SIGNAL

What Changed This Week (Jan 17–23, 2026)

Region: South America + Caribbean

🌍 Trade Is Re-Routing — With Friction

Signal: The EU–Mercosur free trade agreement was signed, while regional tariffs inside Latin America rose.

Why it matters:

Trade gravity is shifting fast — opening markets at the bloc level while raising near-term compliance and political risk.

What happened:

- EU and Mercosur (Argentina, Brazil, Paraguay, Uruguay) signed a deal set to remove 90%+ of tariffs over time.

- Ecuador announced a 30% tariff on Colombian goods starting Feb 1.

Where:

South America ↔ Europe; Ecuador–Colombia border trade.

Who’s hit first:

- Ag exporters (beef, soy, wood pulp)

- Importers of EU machinery & auto parts

- Customs brokers and compliance teams

Confidence: High (deal signed; outcomes hinge on ratification)

Watch next:

- EU parliamentary/legal steps and side-letter demands

- Colombia’s response to Ecuador’s tariff move

💸 Financial Rails Are Fragmenting (Venezuela)

Signal: Control over Venezuela’s oil export revenues shifted toward the U.S., disrupting debt repayment and settlement routes.

Why it matters:

Unclear payment priority raises transaction risk premiums and complicates oil-for-debt mechanisms (notably with China).

What changed:

Oil revenues are routed through managed accounts, altering who gets paid — and when.

Where:

Venezuela (spillovers across commodity and finance networks)

Who’s hit first:

Commodity traders, banks, insurers, shipping firms, governments in restructuring talks.

Confidence: Medium–High

Watch next:

Creditor disputes, legal challenges, and shipment rerouting.

⚡ Energy Stress Is Structural (Not Shortage)

Signal: Brazil’s renewables boom is creating grid balancing and transmission strain.

Why it matters:

Risk has shifted from “not enough power” to “can’t move power efficiently,” affecting reliability and pricing for industry.

What changed:

High solar/wind growth increased curtailment and operational complexity.

Where:

Brazil

Who’s hit first:

Heavy industry, data centers, utilities, project developers.

Confidence: Medium

Watch next:

Curtailment rates, transmission upgrades, market rule changes.

Solutions signal:

Puerto Rico clinics expanded solar + storage, boosting care continuity during outages.

🚚 Supply Chains Under Acute Stress (Haiti)

Signal: Haiti’s political and security crisis intensified, threatening ports, roads, and last-mile delivery.

Why it matters:

Disruptions hit fuel, food, and medical supply flows, raising prices and humanitarian risk.

Where:

Haiti (Caribbean spillover)

Who’s hit first:

Households, NGOs, hospitals, importers, logistics providers.

Confidence: High

Watch next:

Feb 7 political transition deadline and security force scale-up.

🧠 Semiconductor Pressure Is Indirect — But Real

Signal: No local chip shock, but global strategic-tech controls are tightening, raising import costs and lead times.

Why it matters:

Longer delays affect telecom upgrades, fintech infrastructure, and industrial automation.

Where:

Region-wide (import-dependent economies)

Who’s hit first:

Telecom operators, OEM importers, utilities needing advanced spares.

Confidence: Medium

Watch next:

OEM allocation shifts and distributor pricing.

☁️ Compute & Cloud Sovereignty Is Rising

Signal: Venezuela’s hydrocarbons reforms and renewed services interest imply rapid digital modernization — with cyber risk trailing close behind.

Why it matters:

Cloud + OT integration often outpaces governance, increasing continuity and sovereignty exposure.

Who’s hit first:

Energy operators, vendors, regulators.

Confidence: Medium

🛡️ Cyber Risk Tracks Instability

Signal: Haiti’s instability increases exposure to opportunistic cybercrime (fraud, ransomware).

Why it matters:

Digital outages compound humanitarian and supply-chain fragility.

Who’s hit first:

Hospitals, telecoms, banks, NGOs, government registries.

Confidence: Medium

📏 Standards Are Becoming Trade Gates

Signal: EU–Mercosur momentum accelerates standards, traceability, and customs alignment pressure — even before ratification.

Why it matters:

Compliance readiness becomes a competitive advantage.

Who’s hit first:

Food/ag exporters, autos, chemicals, customs brokers.

Confidence: High

💧 Water & Food Stress Remains a Background Constraint

Signal: Hydro-dependent systems remain vulnerable to drought variability.

Why it matters:

Water stress cascades into power prices, food processing, and household costs.

Confidence: Medium (chronic)

✊ Social Stability Is the Top Risk

Signal: Haiti’s governance turbulence and gang violence are the most acute social stability pressure this week.

Why it matters:

Directly impacts workforce safety, logistics, and humanitarian access.

Confidence: High

📊 Pressure Map — This Week

Rising fastest:

- Social stability (Haiti)

- Supply-chain chokepoints (Haiti)

- Financial rail fragmentation (Venezuela)

Holding steady:

- Energy stress (structural, not acute)

- Water & food stress (baseline elevated)

Most likely spillover path:

Haiti instability → distribution breakdown → shortages & price spikes → wider social stress.

🔭 What to Watch (Next 7–14 Days)

- Haiti’s Feb 7 transition outcome

- Security mission scale-up pace

- Ecuador–Colombia tariff enforcement

- EU–Mercosur provisional steps or legal friction

- Venezuela oil shipment and payment routing changes

🔗 From Risk to Solutions

- Social stability → community continuity & de-escalation

- Supply chains → multi-route logistics & local storage

- Financial rails → resilient payments & escrow clarity